A quick overview of important narrative shifts across some macro assets which Precious Metals should take note of. Even though prices have been extremely contained (Gold in the $1800-1880 range and Silver $21-$22.50 for ~6 weeks now) despite the recent 75bp Fed hike and shock CPI, there have been some sizable moves in cyclical commodities, US Bonds and Stocks worth noting, as stagflation/recession is increasingly priced in.

Summary: Gold remains in a mild bull market awaiting a (new) catalyst to break this tactical $1800-1880. There are many supportive macro reasons to own it, but the carnage in stock markets and other asset classes have kept the marginal player at bay. There are better bullish opportunities in Gold-crosses vs XAU-USD given the resilience of the US$ as both a haven and proxy for relatively faster Fed hikes. Tactical bearish risks are growing IF the Fed remains too hawkish vs the further rollover in commodities pricing and higher US$; that would mean a super tightening cycle

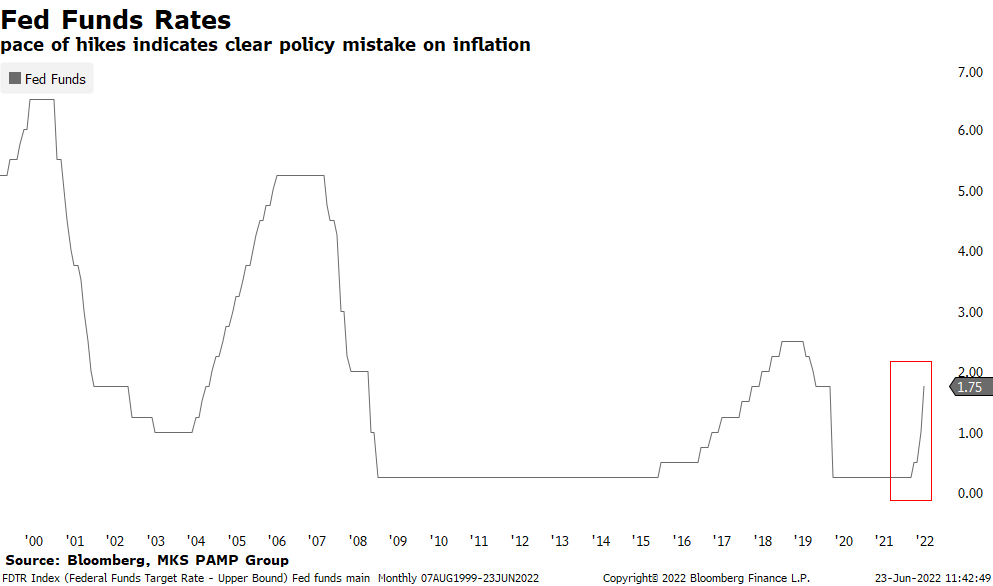

Late take on FOMC: Fed funds is ONLY 1.75% (with CPI at 8.6%). Last week the Fed did what they should’ve (acknowledged inflation & took the over on 50 vs 75bp hikes) but yields have essentially erased most of their move up triggered last Monday / July 10th by the surprise 75 bps hike talk (the coordinated leak ahead of Wednesdays Fed meeting). Overall, the details of the Fed statement were pretty dovish (they have acknowledged the economy is worsening) and recession talk has grown as data continues to disappoint and commodity pricing responds to demand destruction fears. Chart 1 shows the “hockey stick” technical formation of Fed hikes indicating a CB policy mistake on inflation in the simplest form

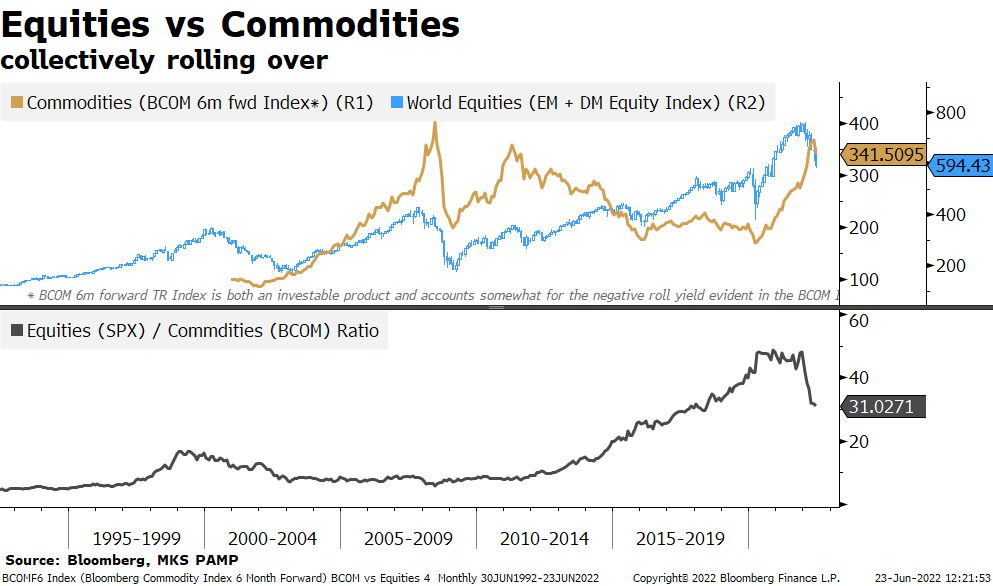

Recession: there are now everyday signs that markets’ fears are shifting from inflation to recession. Today, the sentiment wasn’t helped much by lousy PMI data. Specific consumer & inflation-sensitive sectors like travel are still June’s largest decliners and are the poster child for the soaring inflation & strained consumer. Cyclical & agriculture commodities have rolled over with Copper taking a dirt nap, currently ~$8500/mt (down >20% since pre-invasion peak and extending through YTD lows) while Ali is at $2500/mt down 38% from its 2022 peak. Interestingly Ag commodities are also drawing down while supply bottlenecks in Ukrainian ports have not eased; demand destruction is trumping supply-side constraints. Precious is holding up vs renewed recession fears on a relative basis vs other commodities but it isn’t seeing much broad-based subscription or a rotation away from utility commodities (“reflation”-sensitive) to precious metals (“stagflation”-sensitive)

Commodity prices vs inflation expectations: they have been the driving force behind rising inflation expectations and why there's been persistent MoM CPI prints. But if the Fed is focused on / looking at bringing CPI or PCE down, that is one of the last metrics to rerate in an economic cycle/slowdown. To get inflation and the macro backdrop right, one should get commodities right, and if the Fed continues to hike at +-50bp clips into pressured commodities prices and a lofty US$, that’s an added form of monetary tightening; that would be a huge tightening cycle and behind the bearish Gold narrative (or at the very least explains the hesitancy of broad-based investor subscription).

Oil: Demand destruction (despite the Ukraine war) is also playing out in energy with WTI repricing from ~$125 to $105/bbl in 10days. Overall, the extremely consensual long oil trade has also been the ‘anti-gov trade’ (not gold). The thinking is that global governments are incompetent and are driving up inflation so ‘liquid gold’ / oil is the preferred (inflation) hedge. While short-term repricing lower in oil is due to recession fears, the irony is that Big Oil has 1st been politically vilified (due to energy transition ambitions) and now is the convenient scapegoat for higher gas prices by US politicians. Simply, “nationalization risk” is up (it started with talk/threats around windfall profit taxes) but if overall visibility into politics is murky it makes it tougher to hire & invest and expand oil production in the medium/long-term. That plays into the thesis of structurally higher energy floors and thus a structurally higher interest rate regime vs the past decade+ regime of lower interest rates thanks to China/globalization.

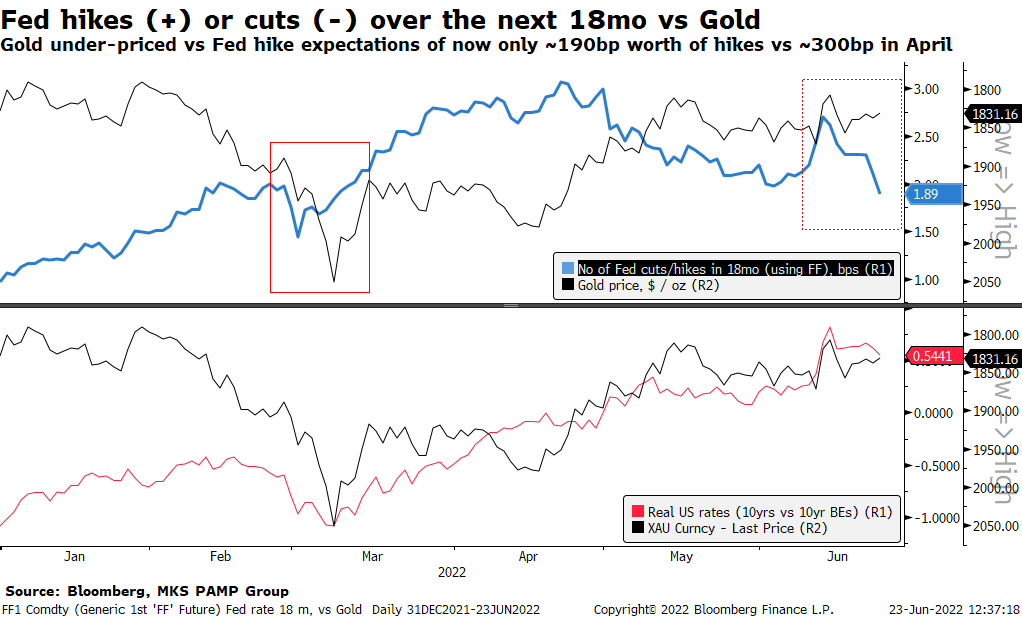

Bonds (& to lesser degree Gold) calling the Feds bluff: The Fixed Income market is indicating that we wont get to lofty (scary) nominal yields before a recession. The Feds Funds terminal rates (priced by the bond mkt) indicates we wont reach 4% Fed Funds (priced 1mo ago) nor even the 3.8% (that the Fed priced at the last FOMC meeting). Eurodollar Dec22/Dec23 spread is indicating that the Fed will CUT 50bp in 2023! Yesterday, Powell testified (it is still ongoing today) that he wont rule out 100bp of hikes but some bond market metrics are indicating they should be cutting, not hiking and certainly challenging the consensual (and Fed view) to remain hawkish.

Stocks: With the sell-off last week in the SPX, its correction is now in line with the median correction seen in post-WWII recessions, but its now the 4th worst ‘non-recession correction’ over the same period. We are in a market recession. Technically, SPX entered a bear market on June 13, making it the 20th bear market over the past 140 year; with average duration at ~290 days; then today's bear market would end in mid October 2022 (IF history is a guide of future performance). The irony and counter-intuitive thinking for gold bulls is prices likely need a combination of lower yields (check) AND higher US equities for prices to push through and retest $1880 levels. There's has been unprecedented damage in equities (and other assets) where money has retreated into cash/US$, less so havens. Confidence needs to return.

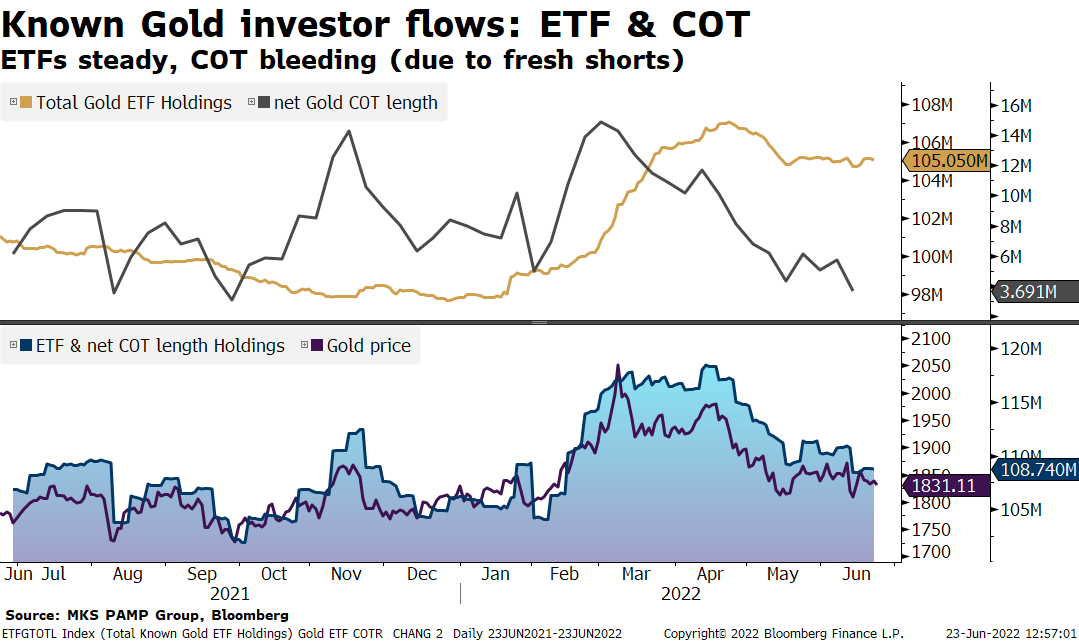

Gold Investor Positioning: There's a notable lack of interest from the investment community (outside of retail coin/bars!). 1m implied gold vol below 20, daily volumes (lackluster), and overall sideways-lower ETF+COT positioning, all indicate no sense of urgency to buy gold in the mid $1800s. The well-accepted belief is that there's plenty of buyers at $1900, not $1800.

Gold catalysts and/or potential indicators to monitor for Gold to break $1800-1880 which opens up ~$2000 target high or $1750 target low

Bullish: through $1880 inflection point:

The big Fed tightening will “break something” – they almost always do.

Wall Street recession triggers a Main Street recession given unprecedented retail interest

US Housing Market: Mortgages are at 6% (average 30-year fixed mortgage rate), and its highest level since 2008. While home builders are reining in construction despite a lack of supply, there's an underappreciated fact that the Fed is QTing (buying LESS Mortgage Backed Securities), with mortgage rates already up here. The MBS market is showing signs of stress (volatility & spreads widening); its widely accepted that if you crash housing (the economic backbone) the economy crashes.

Further signs of a consumer slowdown: jobless claims have surged since April, credit cards are at 20% - the Fed is already having an impact

Food & energy crisis leading to widespread protests and uprisings: Gold cares less about already shaky smaller EM economies (Ecuador, parts of Africa), but any unrest in larger BRICS nations and/or the West is more significant.

Credit event: consensus trades have been long US$$, long Commodities (already unwinding), the few longs left in Tech, all of which are most vulnerable to any credit event

Bearish: through $1800 floor

No ‘new catalysts’: if war risk, inflation risk and recession risk keep quietly persisting, the lack of new bullish drivers usually precedes a tactical repricing lower. If it can’t go higher…

Persistently hawkish Fed into falling inflation expectations: lower Breakeven prices as commodities rollover further will lead to higher real rates and the unlocking of gold holdings (including CB and others large physical holders)

Upcoming event risk

June 26th G-7 summit. June 29th NATO summit,

June 30th PCE deflator

July 8th US payroll

July 13th US CPI (and Biden visits Saudi Arabia)

July 21st BoJ & ECB meetings

July 27th FOMC

July 28thUS Q2 GDP (this could confirm a “recession”)

Make informed decisions on your wealth preservation, by staying informed with news delivered from PAMP.

Shop The Range

Share

Author

MKS PAMP

About MKS PAMP

With a global footprint and over 60 year of experience in the precious metals industry, MKS PAMP – part of the MKS PAMP Group – is dedicated to creating a sustainable future with precious metals products and services. The company offers the world’s most extensive range of durable, innovative and responsibly sourced precious metal products and services. The company builds on leading artisan savoir-faire and Swiss engineering to manufacture a wide range of products in all four precious metals and in various forms, and provides precious metals services such as trading, refining, vaulting and storage, treasury and mine financing.